Choosing between a bridge loan and a permanent loan is one of the most consequential financing decisions you will make on any commercial real estate deal. Get it right, and your capital structure supports the business plan from close to exit. Get it wrong, and you can find yourself paying bridge pricing on a property that could have qualified for permanent financing from day one, or worse, approaching maturity on a bridge loan without a viable takeout in place.

The right loan type is not determined by property class or asset type; it is determined by your business plan, your transition timeline, and your exit strategy.

Most borrowers come into this decision focused on rate. Rate matters, but it is rarely the deciding variable. A 200-basis-point spread between bridge and permanent pricing is far less consequential than the risk of not being able to refinance out of a bridge loan when the term expires. The smartest financing decision starts with the end in mind.

Key Takeaways

The correct loan type depends on whether your property requires a transition period before it can support permanent financing.

Bridge financing carries costs well beyond rate, including extension fees, rate caps, and takeout risk that must be planned from day one.

Permanent lenders are often more flexible on occupancy and stabilization than borrowers assume, which means some deals skip the bridge entirely.

How The Two Loan Types Differ

Bridge loans and permanent loans serve different phases of a property's lifecycle. The core distinction comes down to duration, pricing structure, and what the lender underwrites when approving the deal.

What A Bridge Loan Is Designed To Do

A bridge loan is short-term financing, typically structured for 12 to 36 months, designed to carry a property through a period of transition. The loan is almost always interest-only, which preserves cash flow while you execute a value-add plan, lease up vacant space, or reposition the asset for a sale or refinance.

Bridge loans carry higher interest rates than permanent loans because lenders are taking on transitional asset risk. The property does not yet perform at the level required for long-term debt, so the lender prices for that uncertainty. Loan terms on bridge debt are shorter, leverage can be higher, and the underwriting focuses heavily on the sponsor's execution track record and exit plan.

What A Permanent Loan Is Designed To Do

Permanent financing is long-term financing built around in-place cash flow. It is designed for stabilized assets with documented income, established occupancy, and a borrower who intends to hold for years rather than months. Loan terms typically range from 5 to 30 years depending on the lender type and product.

Permanent loans use full amortization schedules or partial amortization with balloon payments, and they carry lower interest rates because the risk profile is materially different. Lenders underwrite to actual net operating income, not projected income. Cost efficiency over time is the primary advantage.

The Fastest Side-By-Side Comparison

Feature

Bridge Loan

Permanent Loan

Term

12 to 36 months

5 to 30 years

Structure

Interest-only

Amortizing or partial I/O

Rate

Higher

Lower

Underwriting basis

Projected/transitional cash flow

In-place, stabilized cash flow

Leverage

Often higher

Typically more conservative

Primary use

Value-add, lease-up, repositioning

Stabilized acquisitions, refinances

Prepayment flexibility

Usually more flexible

Often subject to yield maintenance or defeasance

The right product depends on where your property sits on this spectrum today, not where you hope it will be.

Choose Based On The Business Plan

The business plan tells you everything. Whether your property needs bridge debt or qualifies for permanent debt comes down to cash flow stability, the length of any required transition period, and what the exit looks like once the work is done.

When A Transition Period Makes Bridge Debt Logical

If the property needs time, bridge debt is logical. A transition period is any window during which the asset cannot yet support permanent financing, typically because occupancy is too low, leases are too short, or a capital improvement plan has not yet been completed.

Transitional assets, by definition, do not meet the stabilization thresholds permanent lenders require. If your business plan calls for leasing vacant space, renovating units, improving physical occupancy from 60% to 90%, or repositioning a property from one use to another, a permanent lender will decline the deal. The property value has not been created yet, and the income stream that justifies long-term debt does not exist yet.

Bridge debt gives you the runway to complete the plan without the pressure of a long-term lender enforcing stabilization covenants. The trade-off is cost. You will pay for that flexibility with higher rates, extension fees, and a rate cap requirement on most floating-rate structures.

When In-Place Performance Supports Permanent Debt

Not every transitional-looking property actually needs bridge financing. If your asset is generating consistent cash flow and the occupancy is sufficient to support the debt service on a permanent loan, a permanent lender may still close the deal.

An 80% occupied retail property is a good example. Many borrowers would assume bridge financing is the only path. But if the in-place tenants are credit-quality and the net operating income covers the debt service at the loan-to-value target you need, a permanent lender may underwrite comfortably at that occupancy level. You avoid the cost and complexity of leasing the remaining space just to satisfy a threshold that may not actually be required.

The key question is whether the cash flow supports the LTV target today. If it does, the stabilization work may not justify the added expense of bridge financing.

How Exit Strategy Drives The Right Choice

Your exit strategy is not a final-chapter decision. It has to inform the capital structure before you close. If the exit is a sale, you need to know whether the projected property value at stabilization justifies the bridge debt cost and leaves meaningful equity. If the exit is a refinance into permanent debt, you need to size that takeout from day one.

Knowing what the permanent lender will require at refinance, how they will underwrite, and what proceeds they will lend tells you whether the bridge execution is viable. If you cannot clearly define that path before closing on the bridge, the deal carries more refinance risk than most borrowers acknowledge. The exit strategy is the filter; everything else follows from it.

When Bridge Financing Makes Sense

Bridge financing is the right tool when the business plan demands it, not by default. The clearest use cases share a common thread: the property cannot qualify for permanent financing in its current state, and there is a defined plan to change that within 12 to 36 months.

Value-Add And Lease-Up Deals

Value-add acquisitions and lease-up plays are the most common use cases for bridge financing. If you are acquiring a property with significant vacancy, deferred maintenance, or below-market rents, permanent lenders will not underwrite to the projected cash flow. Bridge debt funds the acquisition and, in many structures, reserves for capital improvements as part of the loan.

Higher leverage is often accessible through bridge lenders, which makes these deals workable when equity is limited. The capital stack on a value-add deal typically includes the bridge loan as the senior debt with the lender holding back improvement funds in a controlled escrow, reducing upfront carrying costs.

The discipline required is executing the capital improvement plan on schedule. Every month of delay is a month of bridge pricing, and slippage can erode the returns the deal was underwritten to generate.

Time-Sensitive Acquisitions And Auction Purchases

Auction purchases and other time-sensitive acquisitions require closing speed that permanent lenders typically cannot match. Permanent lenders need time to complete underwriting, appraisals, title review, and committee approval. That process takes weeks to months.

Bridge financing can close in days to weeks with less documentation and a more flexible underwriting process. For real estate investors competing in auction environments or off-market deals with short due diligence periods, bridge debt is often the only tool that can execute within the required timeline.

The cost of closing on time is real: higher closing costs, origination fees, and interest rate exposure. But the cost of losing the deal is typically higher.

Maturing Debt And Bridge To Permanent Execution

Sometimes bridge financing is the answer not because of a value-add plan, but because existing debt is maturing and the property is not yet ready for permanent financing. Rescue capital and loan structure extensions fall into this category.

A bridge-to-permanent execution is a deliberate strategy: use short-term bridge debt to stabilize the asset, then refinance into permanent financing once the stabilization thresholds are met. The risk in this execution is assuming the permanent lender will be available at the projected terms when the bridge matures. Extension fees, market rate changes, and lender appetite shifts can all compress the economics. Sizing the takeout before the bridge closes is the only way to manage that risk responsibly.

When Permanent Financing Is The Better Fit

Permanent financing is not the fallback option; it is often the most cost-efficient and appropriate structure for assets that are already performing. Knowing when you qualify, and which permanent lender fits your deal, is as important as knowing when you do not.

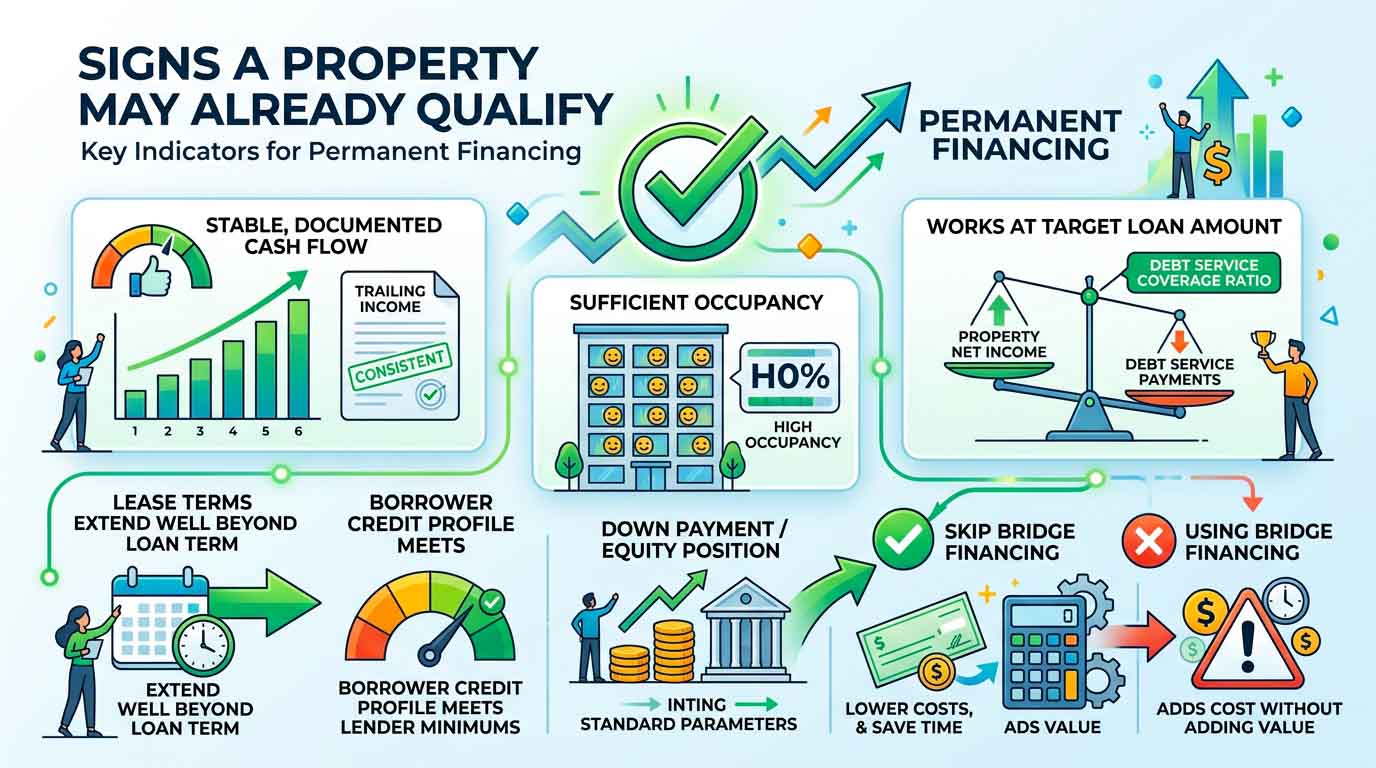

Signs A Property May Already Qualify

The clearest sign that a property qualifies for permanent financing is stable, documented cash flow at sufficient occupancy. Permanent lenders underwrite to in-place performance, so if the trailing income is consistent and the debt service coverage ratio works at your target loan amount, you likely have options.

Other qualifying indicators include lease terms that extend well beyond the proposed loan term, a borrower credit profile that meets lender minimums, and a down payment or equity position that brings leverage within standard permanent loan parameters. If all of these align today, using bridge financing adds cost without adding value.

Why Long-Term Debt Works For Stable Income

When a property generates predictable income over a multi-year hold, permanent financing matches that income profile precisely. Fixed-rate permanent loans eliminate floating-rate exposure and provide a known debt service number for the life of the loan. That certainty supports long-term hold business plans where cash flow projections need to be reliable.

Lower interest rates on permanent loans improve cash-on-cash returns meaningfully over time. On a five-year hold at scale, the difference in interest cost between bridge and permanent debt can represent hundreds of thousands of dollars. For stabilized assets, that gap is difficult to justify.

Comparing Banks, CMBS, And Other Permanent Lenders

Different permanent lenders suit different deal profiles. The table below compares the most common options.

Portfolio lenders with local market knowledge; recourse often required

CMBS Lenders

Larger non-recourse loans, longer terms

Rigid underwriting; prepayment penalties via yield maintenance or defeasance

Life Companies

High-quality, stabilized assets

Competitive rates; conservative LTV; selective on property type

Credit Unions

Smaller deals, owner-occupied

Relationship-driven; limited in scale and geography

CMBS lenders offer non-recourse traditional financing at competitive fixed rates, but the lack of flexibility on prepayment and loan modifications is a real constraint. Banks and portfolio lenders provide more flexibility but with recourse exposure. Matching the permanent lender to the deal profile requires knowing your hold period, exit flexibility needs, and leverage requirements before you start the process.

Underwriting, Risk, And Borrower Readiness

Lenders on both sides of this decision are evaluating different things when they underwrite. Knowing what each side looks for helps you present your deal in the strongest possible light and avoid structure mismatches that create problems after closing.

What Lenders Review Before Approving The Deal

Bridge lenders underwrite to the business plan. They want to see the sponsor's track record on similar transitional assets, a clear renovation or lease-up timeline, a defined exit strategy, and enough equity in the deal to absorb execution risk. Property value at stabilization is central to the analysis because it determines whether the takeout can repay the bridge.

Permanent lenders review the actual operating history. They examine rent rolls, trailing income statements, lease abstracts, and expense records. They want consistent cash flow with coverage at or above their debt service coverage ratio minimum. The property value and loan-to-value drive maximum proceeds.

How Credit, DTI, And Proceeds Affect Terms

Credit score and debt-to-income ratio are more consequential in permanent loan underwriting than in bridge loan underwriting. Permanent lenders, particularly banks and agency-adjacent programs, apply stricter credit thresholds because the relationship extends over years, not months.

For bridge loans, leverage and cash flow reserves typically matter more than credit score alone. Higher leverage will increase pricing. If proceeds must be maximized to satisfy capital stack requirements, expect rate and fee adjustments that reflect the added risk to the lender. Optimizing closing costs, loan terms, and proceeds requires knowing where each variable creates constraint for your specific deal.

Mistakes That Create Refinance Risk Later

The most common mistake is closing on a bridge loan without having sized the permanent takeout first. If the bridge proceeds create a loan balance that the stabilized net operating income cannot support at permanent financing LTV targets, the exit does not work on paper before you even start executing the plan.

Using traditional financing assumptions that do not match the actual lender environment at refinance is equally risky. Debt markets shift. If your underwriting assumed a permanent lender at 6% and rates move to 8% by the time you are stabilized, the takeout proceeds drop materially. Stress-testing the takeout before closing on the bridge loan is not optional; it is the core discipline of responsible bridge execution.

A Practical Decision Framework Before You Commit

Before you contact a lender, spend time stress-testing your own deal against the key variables. Cost efficiency, exit strategy clarity, and lender alignment are all decisions you can shape before the process starts, not after.

Work through these questions before you pick up the phone:

Does the property generate enough in-place cash flow to support permanent financing today?

If not, what specifically needs to change, and how long will that realistically take?

What is the exit: a sale or a refinance into permanent debt?

If the exit is a refinance, what will the permanent lender require on occupancy, lease term, and debt service coverage?

Can you quantify the cost of bridge financing, including rate, origination, extension fees, and rate cap, and verify the return still works after those costs?

What happens if stabilization takes 6 months longer than planned?

If you cannot answer each of these clearly, you are not ready to commit to a bridge loan yet.

How To Size The Takeout Before Closing

Sizing the takeout means working backward from the stabilized scenario to confirm the bridge is supportable. Start with a realistic stabilized net operating income estimate based on market rents and achievable occupancy. Apply the permanent lender's underwriting criteria: their minimum debt service coverage ratio, their maximum LTV, and their applicable interest rate.

The resulting loan amount from the permanent lender needs to cover the expected bridge balance at payoff, including any accrued fees. If it does not, you either need to contribute additional equity at stabilization or restructure the bridge proceeds downward. Doing this math before closing eliminates the most damaging structural mistake in bridge financing.

Frequently Asked Questions

A bridge loan is short-term financing, typically 12 to 36 months, used to carry a property through a transition period until it qualifies for long-term debt or is sold. A permanent loan is long-term financing based on stabilized, in-place cash flow, typically used for properties that are already performing. The two products serve different phases of a property's lifecycle, not the same phase.

Short-term financing makes sense when the property cannot qualify for permanent debt in its current state, usually because occupancy is too low, leases are too short, or a capital improvement plan has not yet been completed. It also applies when acquisition timelines are too tight for a permanent lender's process, such as auction purchases or off-market deals with rapid closing requirements.

Bridge loans are typically offered by private lenders, debt funds, and select commercial banks. Eligibility requirements vary but generally include a track record on similar deals, a viable exit strategy with a clear stabilization timeline, sufficient equity or down payment in the deal, and a realistic property value at stabilization that supports repayment. Credit score thresholds tend to be more flexible than with permanent lenders.

To estimate total cost, you need the loan amount, the interest rate, the interest-only payment period, expected origination fees, any required rate cap premium, and estimated extension fees if the plan runs long. A basic model multiplies the loan balance by the annualized interest rate, adds origination and rate cap costs at close, and layers in extension fees if the term goes beyond the initial period. Running this against your projected stabilized value and takeout proceeds tells you whether the deal returns what you modeled.

Bridge loan rates are materially higher than permanent loan rates because they reflect transitional asset risk, shorter terms, and reduced documentation requirements. In practice, bridge rates often run 200 to 400 basis points above comparable permanent financing depending on leverage, asset type, and market conditions. Fees are also higher: origination costs, rate cap premiums, and extension fees add to the total cost in ways that a simple rate comparison does not capture.

For commercial real estate deals involving transitional assets, a bridge loan is typically more appropriate than a HELOC or a swing loan because those products are designed for residential or smaller-scale use cases. A HELOC draws on existing equity in a primary residence; a swing loan is a short-term residential product for buyers moving between homes. Neither is structured for the leverage levels, loan sizes, or transitional asset profiles common in commercial real estate. If your deal involves a CRE property at any meaningful scale, a purpose-built bridge loan from a commercial lender is the more relevant comparison.

At Dena Capital, we revolutionize the commercial real estate industry by investing in our people and technology to deliver unmatched client experiences and maximize value.